Table of Content

Typically, homeowners choose a $1,000 deductible , with $500 and $2,000 also being common amounts. Though those are the most standard deductible amounts selected, you can opt for even higher deductibles to save more on your premium. It's important to understand what you're responsible for paying when you enter into an insurance contract. Depending on the coverage you have, you may have both a deductible and an out-of-pocket maximum. Fortunately there are some key differences to help you tell these apart. There’s no such thing as the perfect deductible for every policy.

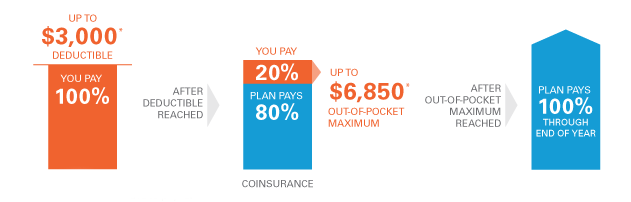

Once you reach your out-of-pocket maximum, your insurance plan will pay all additional expenses at 100 percent. You’ll continue to pay premiums until you no longer have the insurance plan. A deductible, on the other hand, only has to be paid if you use the insurance. Your deductible automatically resets to $0 at the beginning of your policy period.

What should you not say to an insurance adjuster?

Is often sold as a package that covers several possible predicaments, such as trip cancellation, loss of your baggage and emergency medical treatment. We believe everyone should be able to make financial decisions with confidence. By choosing a $2,000 deductible over a $500 one — according to ASI Progressive rates. This article has been reviewed by a licensed Policygenius expert to ensure that sources, statistics, and claims meet our standard for accurate and unbiased advice. Between 10,000 and 15,000 miles per year is what's considered average.

A 2 percent windstorm deductible means you’ll pay $6,000 of your own money. But while this makes sense from a financial standpoint, paying a low deductible often results in higher insurance premiums. But while keeping your premium up-to-date insures coverage, home insurance policies don’t provide 100 percent coverage. Some policies have a flat deductible for homeowners insurance, and others use a percentage.

Frequently Asked Questions (FAQs)

A deductible waiver might also be required to achieve a zero deductible. First consider how much this option might increase your premium costs. The content on this page is for general information purposes only and does not constitute legal advice.

This is usually $500 to $2,000, but the deductible can be as low as $250 or higher than $5,000. With flat deductibles, the amount you pay for your deductible stays the same no matter the size of your insurance claim. But a deductible that is too low might mean paying more premium than you want to. Typically, insurance agents recommend that your comprehensive deductible be between $100 and $500. Comprehensive claims tend to be filed for less damage than collisions, so having a lower deductible is often logical. The insurer would then proceed to pay for damages over that amount.

Find Insurance By State

Knowing what all parts of your insurance contract mean can help you get the most out of your coverage. The reason companies have done this is because hurricanes can cause extreme and total damage, resulting in billions of dollars lost. Florida is currently the only state where hurricane deductibles have been dictated by law instead of insurance companies.

When you buy a house, you’ll be required to purchase homeowners insurance. That’s because your mortgage lender wants to be sure their interest in your property is protected in case of a crisis. But what you pay for homeowners insurance depends on several factors, including your deductible. Whatever deductible you choose, make sure you have at least that amount saved should you need to use it. Most standard insurance policies don’t cover earth movement, which includes earthquakes, mudslides and sinkholes. When it comes to sinkholes, one exception may be if you live in Florida, where insurers are legally required to offer some sort of protection from ground cover collapse.

Renters insurance deductible

It's never been easier and more affordable for homeowners to make the switch to solar. Her writing focuses on reporting the best places to live in the U.S. based on certain interests and lifestyles. In Communications from Alma College and has worked as a writer and editor for various publications in Philadelphia, Chicago and Metro Detroit. However, there might be a chance that you can if you work from home or rent out your home. Kara McGinley is a former senior editor and licensed home insurance expert at Policygenius, where she specialized in homeowners and renters insurance. As a journalist and as an insurance expert, her work and insights have been featured in Forbes Advisor, Kiplinger, Lifehacker, MSN, WRAL.com, and elsewhere.

He saved me a lot of money and I will highly recommend this company to any of my colleagues. And bent over backwards to get me Contractors insurance by Midnight. I'm very happy with the service I received and will continue to do business with them in the years to follow. The kind of stuff that hopefully makes you stop and think – and maybe discover something that can help your business, or life. This is either a standard fixed amount, or a percentage of your home’s insured value.

Your home insurance deductible can play an important role in your premium — a higher deductible often translates to lower premiums . If you have a lower deductible, they’ll have to pay out more if you file a claim. Your home insurance deductible is the other side of the coin, and it can have a real impact on your financial health. Let’s take a deep dive into how your homeowners insurance deductible works. Understanding it can help protect your home while saving you money in both the short and long term. Unlike in car or home insurance where the deductible is paid per claim, the deductible in health insurance can be spread out over the year.

In some states, like Texas, the deductible kicks in for any wind or hail storm. For example, Connecticut triggers hurricane deductibles when a hurricane in the state produces winds of more than 74 mph, but in Delaware, a hurricane watch or warning is enough. Disaster deductibles are mandatory in some states, and even if it is not, you may benefit from having one if you live in an area prone to extreme weather events. A disaster deductible is an amount you need to pay after certain events, and it can be different from your regular deductible. Can you deduct these closing costs on your federal income taxes? When it comes to a policy with zero deductible, you'll often be charged a fee for this in exchange, known as a no-deductible fee.

While our articles may include or feature select companies, vendors, and products, our approach to compiling such is equitable and unbiased. The content that we create is free and independently-sourced, devoid of any paid-for promotion. You can also save by continuing an existing relationship with an insurance provider. These deductibles often apply to named windstorms such as hurricanes and tropical storms. Deductibles don’t only impact how much you pay when filing a claim.

No comments:

Post a Comment