Table of Content

- How To Choose Your Deductible

- How to choose your deductible for homeowners insurance

- How do home insurance deductibles affect the cost of insurance premiums?

- How does a homeowners insurance deductible work?

- How your homeowners insurance deductible affects your rate

- Should you choose a higher deductible on health insurance?

- A Guide To Choosing the Best Deductible

Home insurance offers a lot of protections, and it can significantly reduce your out-of-pocket expense. Instead, your deductible is a percentage of your home’s insured value. The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation.

Expenses that don't count toward the out-of-pocket maximum include premiums and costs that aren't covered by your plan. Plans that charge higher premiums may have lower out-of-pocket maximums. For example, a plan with a $1,000 in-network individual deductible might have a $2,000 out-of-network individual deductible. The same plan might have a $2,000 in-network family deductible, and a $4,000 out-of-network family deductible. Meredith Mangan is a senior editor for The Balance, focusing on insurance product reviews. She brings to the job 15 years of experience in finance, media, and financial markets.

How To Choose Your Deductible

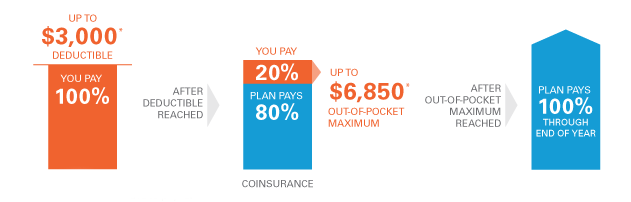

A health insurance deductible is the amount of money you agree to pay for covered services before your health insurance company begins to pay. Once you've reached that deductible, the health insurance company pays a portion of the costs of your care. This is called coinsurance, and it might be split such that the insurer pays 80% and you pay 20%. Instead of a deductible and coinsurance, some plans charge a copayment, or copay, such as $25 or $100, for prescription drugs and office visits.

Our mission is to provide readers with accurate and unbiased information, and we have editorial standards in place to ensure that happens. Our editors and reporters thoroughly fact-check editorial content to ensure the information you’re reading is accurate. We maintain a firewall between our advertisers and our editorial team.

How to choose your deductible for homeowners insurance

If you buy auto and home insurance from the same provider, your homeowners policy might come with a waiver of deductible clause. Typically, the waiver would apply when the same disaster damages your house and your car. There are advantages to using a health savings account paired with a high-deductible health plan, especially if you have a large emergency fund and don't often use health insurance.

If you don’t have a claim, you can end up saving money every month. The risk is that if you do have to make a claim, you might have significant out-of-pocket expenses. So it’s critical to choose a deductible that you know you could afford to pay. But there are opportunities to save money if you understand how insurance deductibles work. Before your insurance company pays you anything, it’s going to subtract your insurance deductible, meaning that some money will likely come out of your pocket. We’ll cover everything you need to know about your homeowners insurance deductible.

How do home insurance deductibles affect the cost of insurance premiums?

Make sure to work with your independent insurance agent to find out if your policy's deductible has a minimum or if the option is available to have zero deductible. Deductible amounts vary depending on the type of coverage you're looking for, such as home insurance or car insurance. The deductible may be a fixed dollar amount or a percentage of your total coverage limit. Often a lower deductible means a higher insurance premium cost, and vice versa. An insurance policy is a type of contract between a customer and insurance company or carrier, in which the carrier agrees to pay for certain covered losses up to the policy's limit. But the customer also has a responsibility in that contract, which is to fulfill the deductible amount on their own.

This content is not provided or commissioned by the bank advertiser. Opinions expressed here are author’s alone, not those of the bank advertiser, and have not been reviewed, approved or otherwise endorsed by the bank advertiser. This site may be compensated through the bank advertiser Affiliate Program. But again, only choose a higher deductible if you have enough cash in reserves.

Rather, they pay for something equal to the deductible amount – car repairs or medical tests, for example – then the insurer pays out for the rest of the coverage up to the maximum limit. For example, if the home suffered $20,000 in damage, the homeowner would need to pay for $15,000 of the repairs before the insurance company pays for the remaining $5,000. After you have met your deductible, your health insurance plan will pay its portion of the cost of covered medical care and you will pay your portion, or cost-share. A health insurance deductible is a specified amount or capped limit you must pay first before your insurance will begin paying your medical costs.

Tend to be lower than homeowners and thus result in cheaper monthly premiums, so raising your deductible may not have the same impact on your overall savings as it does with other coverages. Deductibles are a nearly unavoidable part of most types of insurance. Policies without deductibles do exist, but they typically carry very high premiums. When you make a claim, your insurance deductible is the amount you have to cover yourself before your insurance company will chip in.

Learn how to tackle routine maintenance issues on your own, or to find a competent handyman whom you trust and can easily afford. Many homeowners end up spending about 1 percent of their home’s purchase price on yearly issues. So, if you can, try to put that amount away in a savings account for when issues occur . That said, a higher deductible typically results in lower premium costs, but comes with higher costs out of pocket if you make a claim.

Since your deductible is $1,000, you pay the roofing company $1,000 out-of-pocket before your insurance company covers the remaining $7,000. Another part of assessing the risk of insuring your home is determining how much it’s going to cost the insurer to pay your claims. The more money you’re paying out of pocket, the less your insurer must pay. The standard deductible is a fixed dollar amount, typically in the range of $500 – $2,000. When you have a standard deduction, the amount you’ll pay stays the same, no matter the cost of damage. That means if the cost of damage to your home is less than your deductible, the insurance company wouldn’t pay anything.

Knowing what all parts of your insurance contract mean can help you get the most out of your coverage. The reason companies have done this is because hurricanes can cause extreme and total damage, resulting in billions of dollars lost. Florida is currently the only state where hurricane deductibles have been dictated by law instead of insurance companies.

Let’s look at a few examples of how claims and deductibles might work. Otherwise, it’s up to the policyholder and their circumstances. If your claim is for $10,000 and you have a $500 deductible, you’ll receive a $9,500 claim check from your insurer.

No comments:

Post a Comment